Powerfleet (AIOT)·Q3 2026 Earnings Summary

Powerfleet Beats Revenue Estimates, Lands Landmark 100K Vehicle Public Sector Contract

February 9, 2026 · by Fintool AI Agent

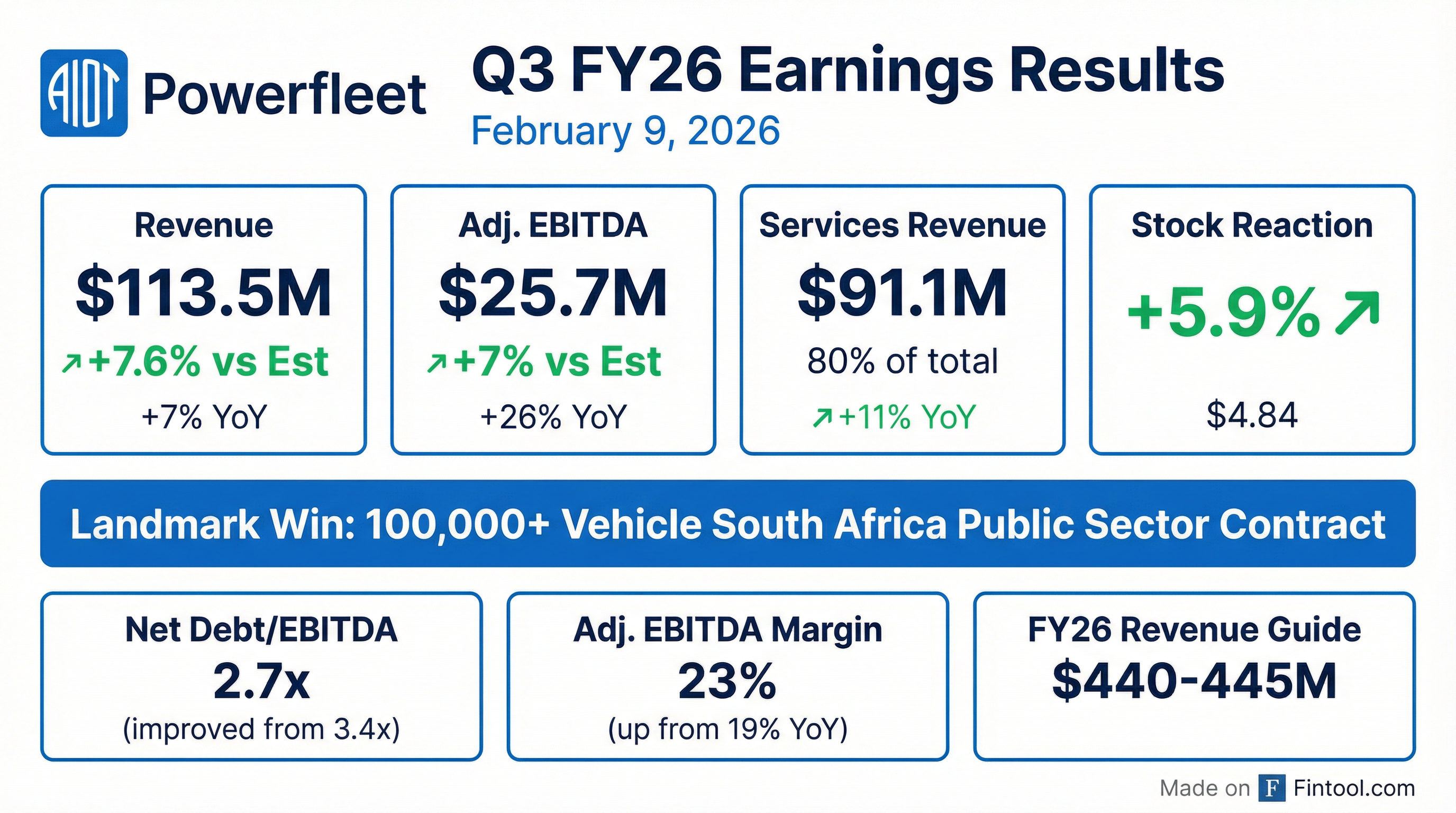

Powerfleet (NASDAQ: AIOT) delivered a strong Q3 FY26, beating revenue estimates by 7.6% with record quarterly revenue of $113.5 million and adjusted EBITDA up 26% year-over-year . The quarter's headline was a landmark South Africa public sector contract covering over 100,000 vehicles — one of the largest wins in company history .

Did Powerfleet Beat Earnings?

Powerfleet exceeded estimates on the top line but delivered mixed EPS results:

The revenue beat was driven by 11% growth in high-value services revenue, which now represents 80% of total revenue (up from 77% in the prior year) . This recurring revenue base is the foundation of Powerfleet's SaaS transition.

GAAP net loss improved dramatically to -$3.4 million from -$14.3 million in Q3 FY25, reflecting operating leverage and cost synergy realization post-merger .

What Was the Major Contract Win?

The quarter's standout announcement was a landmark South Africa public sector contract with MTN to deploy AI video intelligence and real-time fleet visibility services across more than 100,000 government vehicles .

"Our collaboration with Powerfleet supports the rollout of secure, enterprise-grade connectivity for large public sector operations and advances the modernization of critical transport infrastructure." — Tumi Chamayou, Chief Enterprise Business Officer at MTN

CEO Steve Towe characterized the win as a "landmark proof point of Unity's ability to secure large scale wins across mission-critical operations" . Programs of this size typically anchor long-duration customer relationships and create a foundation for additional software and analytics adoption over time .

The contract is expected to begin revenue ramp in the second half of fiscal year 2027, and Powerfleet is maintaining investments in operating expenses to support anticipated material increase in demand .

What Did Management Guide?

Powerfleet tightened FY26 guidance while noting increased investments:

The modestly lower EBITDA and leverage targets reflect "retained investments in operating expenses required to support the anticipated revenue ramp from the more than 100,000 subscriber South Africa public sector opportunity beginning in the second half of fiscal year 2027" .

How Did the Stock React?

AIOT shares rose +5.9% to $4.84 on earnings day, outperforming the broader market. The stock has traded between $3.70 and $8.71 over the past 52 weeks.

The positive reaction suggests investors focused on the landmark contract win and revenue beat rather than the EPS miss, which was driven by timing of investments rather than operational weakness.

What Changed From Last Quarter?

Several key trends continued or accelerated from Q2 FY26:

Improving Leverage Profile: Net debt to adjusted EBITDA improved to 2.7x from 2.9x last quarter and 3.4x at fiscal year-end 2025 . The company remains on track to achieve approximately one full turn of deleveraging by March 2026.

Margin Expansion Continues: Adjusted EBITDA margin expanded to 22.6% from 19.8% in Q2 and 19.2% in Q3 FY25 . G&A expense as a percentage of revenue declined to 23% from 27% YoY .

Services Mix Accelerating: Services revenue as a percentage of total revenue reached 80%, up from 78% in Q2 and 77% in Q3 FY25 .

Key Enterprise Wins

Beyond the South Africa contract, Powerfleet announced significant enterprise expansions in Q3 :

The company also highlighted AI video adoption expanding across major global accounts including Fortune 500 companies in building materials (18 countries, 9,000 assets), industrial gas (19 countries), energy (60+ countries, 15,000+ assets), and mining (3 continents) .

Customer Case Study — Origin Energy: Management highlighted a 14-year customer relationship with Origin Energy, operating 2,000 vehicles. Through phased multi-product deployment from compliance to advanced AI video, Origin achieved "consistent reductions in risky driving events and enhanced their public reputation as a direct result of the safety improvements Powerfleet has driven for them" .

Financial Highlights

Profitability Metrics

Balance Sheet & Cash Flow

Operating cash flow turned positive at $20.5 million for the nine months ended December 31, 2025, compared to cash used of -$16.9 million in the prior year period .

Management Commentary on AI

When asked about AI's impact on the fleet management industry, CEO Towe framed AI as an enabler rather than a competitive threat:

"We see AI as an enabler for our industry. One of the challenges within the industry is it's produced too much data. And then it's been hard for customers to kind of wade through all of that data... The AI abilities we're bringing into the platform allow us to provide very meaningful, simple data to customers that they can access in real time." — CEO Steve Towe

On autonomous vehicles: "Our place remains in people need to understand what those vehicles are doing, where they are, how they're performing... We see that as one as a place where Powerfleet's place in the ecosystem will remain and potentially grow off the back of that."

Risks and Concerns

Investment Spend May Pressure Near-Term Margins: Management explicitly noted that EBITDA guidance was narrowed to ~45% growth (from 45-55%) due to investments needed to support the South Africa contract ramp. CFO David noted they are "trading down of a reduction of costs" by repurposing planned cost savings into growth investments .

EPS Miss: While adjusted EPS improved 100% YoY to $0.02, it missed consensus of $0.04. The company remains GAAP unprofitable with net loss of -$3.4 million .

Contract Execution Risk: The 100,000+ vehicle South Africa contract is transformational but carries execution risk. CEO Towe acknowledged "you have to ramp up in terms of people, process, and systems in order to take that extra weight into the business" . Revenue ramp isn't expected until H2 FY27.

Cash Decline: Cash decreased from $48.8M to $35.9M during the nine months as the company invested in growth and capital expenditures .

Q&A Highlights

On the South Africa Contract Size:

"If you look at bundled solutions and you look at our ARPUs that we get... this contract is within our suite range in both our ARPU and margin. And then you multiply that by the number of vehicles. And we have an ability to do more than 100,000 vehicles. Then I think the math speaks for itself in terms of what this will mean from a recurring ARR perspective for the business over the coming years." — CEO Steve Towe

Management confirmed the South Africa contract will become the company's single largest contract once fully implemented .

On Contract Mechanics: The contract is led by South Africa's National Treasury with fixed pricing already established. Enrollment is opt-in by government departments (not mandated), but CEO Towe noted enrollment has been "super strong" and "stronger than we maybe even imagined it was going to be" .

On FY27 Growth Targets:

"For FY27, I think we've pegged kind of 15% ARR growth. And that's before we kind of think about this new contract and this new opportunity that we have ahead of us." — CEO Steve Towe

On Business Environment: When asked if conditions were better, same, or worse than six months ago, CEO Towe stated: "For us, it's improving... we've been able to find our place to fight and our place to win in the marketplace" .

On Revenue Mix: Management confirmed 65%-70% of business comes from existing customers, with 30% from new logos .

On AT&T Partnership: AT&T sales force will have Powerfleet's full video solution portfolio ready for April 1st following completion of government accreditations .

Pipeline Momentum

The transcript revealed strong leading indicators not covered in the press release:

"Our AI video pipeline build increased 71% sequentially, driven by strong demand for advanced safety, compliance, and visibility solutions across global accounts." — Jeff, Commercial Lead

Data Highway Strategy

Management elaborated on the "Data Highway" strategy — positioning Unity as the connective tissue between fragmented enterprise systems (ERP, HR, TMS, IoT infrastructure) to enable automated, policy-driven operational decisions .

"Unity is becoming embedded at the heartbeat of our customer operations across people, assets, and processes. That makes us increasingly strategic for the customer, highly sticky and difficult to displace." — Jeff, Commercial Lead

Forward Catalysts

- South Africa Contract Ramp: Revenue contribution expected to begin H2 FY27 — potentially the company's largest single contract

- FY27 ARR Growth Target: Management targeting 15% ARR growth before South Africa contract impact

- AT&T Sales Enablement: Full video portfolio available to AT&T reps starting April 2026

- Continued Deleveraging: Target of 2.4x net debt/EBITDA by March 2026

- AI Video Adoption: 71% sequential pipeline build suggests continued momentum

Data sourced from Powerfleet Q3 FY26 earnings call transcript, earnings release, and investor presentation dated February 9, 2026. Estimates data from S&P Global.